eDreams: Disproving the Bears and Regaining Credibility

Business Model is Intact and Management is Hoovering Up the Stock

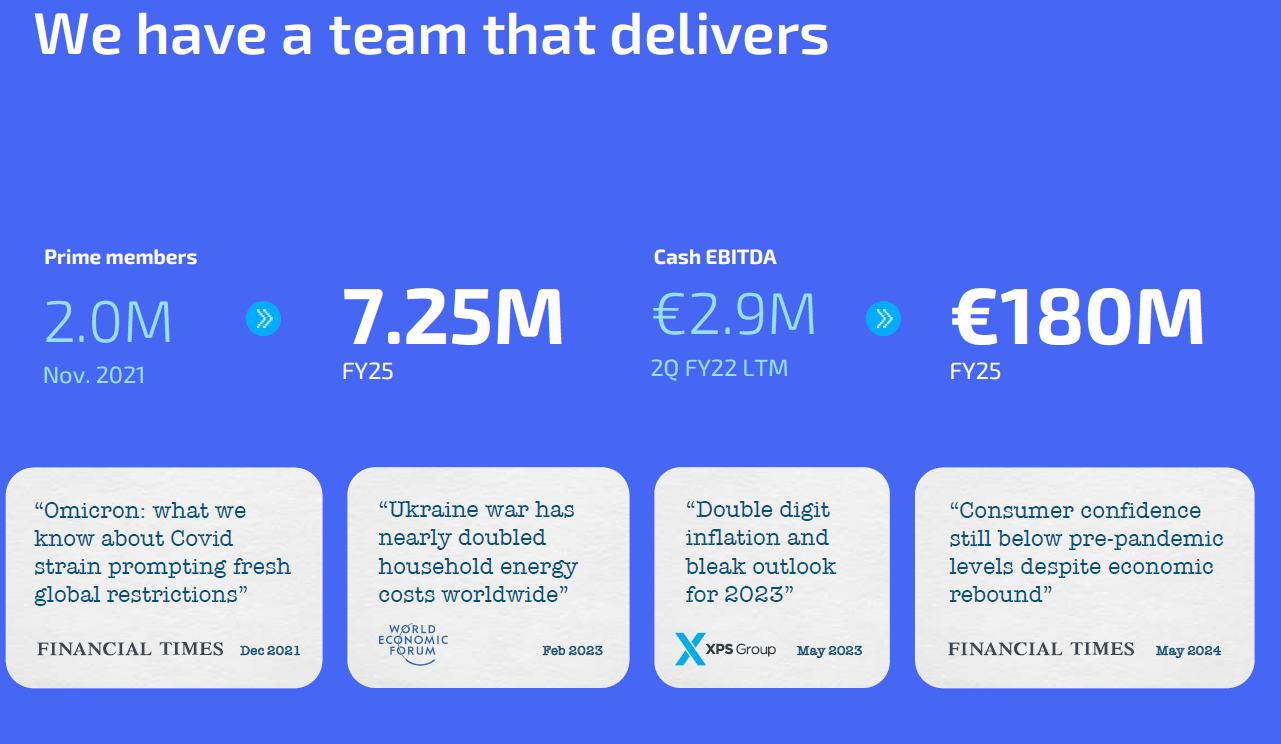

Last year eDreams was flying high. Early in 2025, they held a Capital Markets Day which was the capstone to the goals set at the previous Capital Markets Day (“CMD”) in November of 2021. Between the two CMDs management grew the Prime program to 7.25M members from 2.0M members and increased eDreams’ Cash EBITDA to €180M from €2.9M. Management accomplished these feats despite significant headwinds (Omicron variant of COVID restarting some lock downs, Ukraine War, double-digit inflation, high interest rates, etc.). In achieving their goals, they transformed eDreams business model from transaction based to subscription based (for the importance of this, see (1) and (2)). Pre-COVID only 5% of their revenue came from Prime Subscriptions. At the November ’21 CMD the number had grown to 38% and by October 2024 it had grown to 66%. At the January ’25 CMD, management set out new financial targets for growing Prime members +1M in FY26, then 10% per year for FY27 and FY28. They also set out Cash EBITDA target range of €215M to €220M for FY26.

Not only was the company moving towards hitting their new guidance for most of CY ’25, but also the company was in the market buying stock every day. Then came the turbulence in mid-November. There were several announcements on the second quarter earnings call that spooked the market. Before getting into them, I’d start by saying that eDreams was not priced for perfection going into the call, so the stock price should not have reacted as it did. But bad things happen when you spook the market and your stock has low trading liquidity.

A Turkey Just in Time for Thanksgiving

Ryanair and Its Luca Brasi Approach to OTAs:

The first big announcement was that Ryanair had intensified their online travel agency (“OTA”) blocking efforts, and they were becoming more successful in blocking access to Ryanair content for eDreams. Ryanair previously accounted for ~20% of gross adds for new Prime subscribers. Losing access to that content made it harder for eDreams to achieve its targets for the number of Prime subscribers. Consequently, eDreams lowered its guidance for Prime subscribers for FY26 from the original 1M+ to 600k. It is worth noting that eDreams is fighting for access to Ryanair’s content and that subsequent to the Q2 Earnings Call, the Italian Competition Authority imposed a €256M fine on Ryanair for abuse of its dominant position. The Authority claimed that Ryanair “put in place an elaborate strategy affecting the ability of online and traditional travel agencies to purchase Ryanair flights…. the company’s strategy blocked, hindered or made such purchases more difficult and/or economically or technically burdensome when combined with flights operated by other carriers and/or other tourism and insurance services”. Aside from Ryanair’s blocking efforts, it also implemented a massive smear campaign with labeled “Pirate of the Month” to put additional pressure on OTAs to get OTAs to sign “partnership agreements” that benefited Ryanair, while hurting OTAs and ultimately consumers (for more information see (3)). Consequently, eDreams removed Ryanair transactions and Prime Subscriber additions from all their future financial projections, effectively de-risking their projections to the downside.

Introduction of Monthly/Quarterly Subscription Payments:

Additionally, it had previously been disclosed that for several quarters, eDreams tested monthly and quarterly Prime Subscription Payments (4) in some markets. eDreams found that by having these payment options available, they were able to gain new subscribers, subscribers who for some reason were uncomfortable paying for a Prime subscription upfront for the entire year. Additionally, these payment options led to increased higher customer lifetime values (“LTVs”) and higher net promoter scores (“NPS”).

Introducing New Geographic Markets and Services:

In addition to testing new payment terms, eDreams had been testing Prime in new geographies. They tested Prime in 14 markets that had similar attributes to their top 5 European markets and decided to roll out Prime in 5 new markets: Argentina, Mexico, Poland, South Africa, and UAE.

Additionally, management identified European rail as a new service. This €40B+ with ~330M annual passengers is large and growing, it is deregulating, and it is taking share form short-haul flights.

By entering into more markets and launching new products, eDreams management is continuing its push to be the one-stop shop for travel (more correctly, a one-stop Costco like shop). These moves should make eDreams a more diverse company. If management is successful, then eDreams would not only be more valuable given its strong financial position but also be more attractive to strategic buyers (especially major tech companies wishing to create an “everything” app).

The Financials:

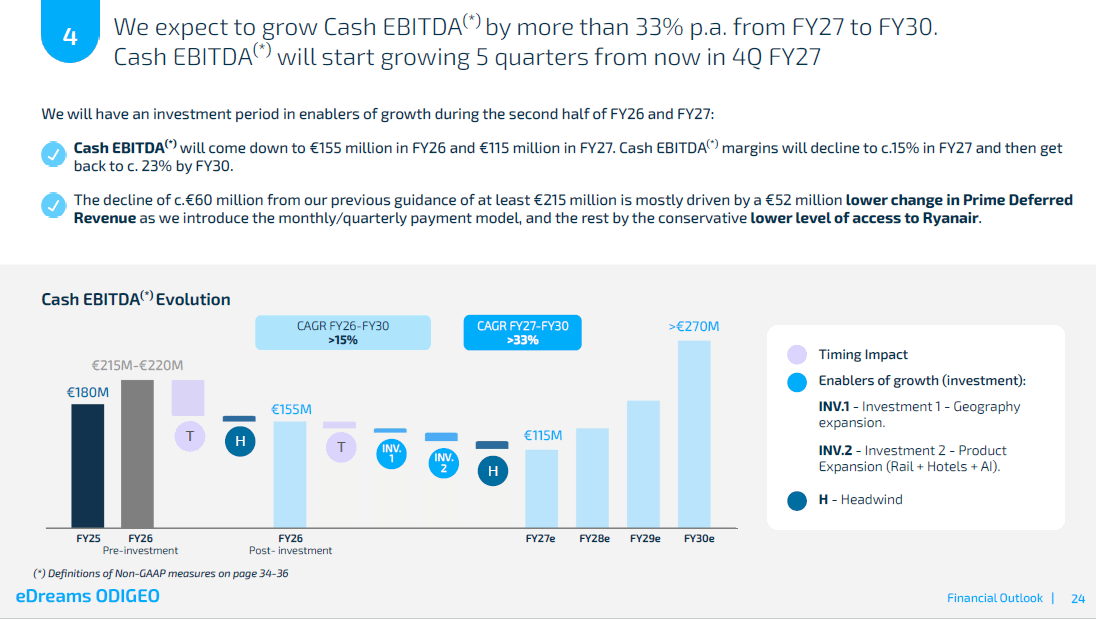

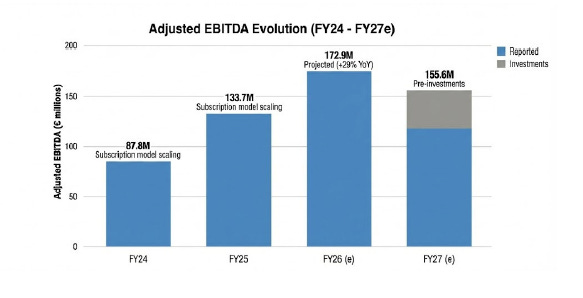

While eDreams laid out 1-year guidance 10 months prior at the FY26 CMD, they laid out new long-term guidance on the Q2 earnings call. There was, however, an unforced error in the presentation of the new estimates. Since the ’21 CMD, management has emphasized the use of “Cash EBITDA” as their main earnings metric. This made sense given the transformation of eDreams into a subscription model and the fact that the Prime subscriptions were one-year subscriptions, paid upfront. With the new monthly and quarterly paid annual subscriptions, the Prime subscriptions would still be one year subscriptions but payments for them would be a mix of annual, quarterly, and monthly paid subscriptions. Hence, there would be a massive working capital draw that would temporarily lower Cash EBITDA but be irrelevant to the company’s earnings and Adj. EBITDA. Management only used Cash EBITDA in setting the new guidance. Management should have shown both Cash and Adj. EBITDA metrics. Additionally, customer-acquisition costs (“CAC”) are higher when you first enter new markets (presumably when you add new products too) and so eDreams’ expansion will require an ample investment. This investment will run through the income statement, making earnings appear lower than they actually are. To their credit, management did recognize this mistake and issued a press release showing the Adj. EBITDA projections and evolution, but at this point, it the damage had been done.

The combination of the speed bump with Ryanair (despite the headwind, Prime subs were still expected to grow), the introduction of quarterly and monthly paid Prime subscriptions, the introduction new markets and services that some could view as a business model pivot, all causing FY26 – FY27 Cash EBITDA to drop ~48% (5), when combined with the stocks low liquidity caused a disaster. Now let’s be real. This is not a 48% drop in true earnings. The biggest reduction is a working capital build, followed by investments. If eDreams was not a subscription company, the investments would be capitalized and amortized over time. The smallest part of the earnings revision is the Ryanair headwind. We will never know, but my gut says that if the Ryanair issue was the only thing that was announced that day, the selloff would not have been as severe. As previously mentioned, the stock was not exactly priced to perfection. But the combination of all these announcements at once spooked investors as they believed the business model may have been broken. The malaise in the stock continued in the first half 2026, as AI disruption fears spread through OTAs and software companies. Today, we are just over six months past the Q2 earnings call and with the benefit of time, we can take a look to see if the business model is broken.

Where We Are Today?

eDreams held their FY26 Q4 earnings call on May 28th. At this point, I believe we can say that the Prime business model is not broken. Additionally, the new products and services are still in their early stages, but there have been some key learning. Let’s start with the financials. Access to Ryanair content has been intermittent. Despite this headwind, the Prime subscribers ended the fiscal year at 7.9M subs – up 8.9% over last year. That means eDreams added 643k net subscribers, which is 43k subscriber higher than their revised estimates from the Q2 earnings release. Adjusted EBITDA (the preferred earnings metric at this point) was €172.3M, up 29% over last year and only €600k lower than the guidance given on post the Q2 earnings call (immediate chart above). As expected, given the working capital change, Cash EBITDA was down 13.0%, but it was €2M higher than the estimates from the Q2 Earnings Release. Adjusted EBITDA Margins where 25.8% for the year vs 19.9% last year. These are not the results of a business with a broken business model. The fact that they came in as close as they did to the estimates in Q2 shows the durability and predictability of the Prime business model.

Regarding the rail product, the first learning the company is seeing is that Prime customers who use it for rail are using Prime more often than non-rail Prime members. This makes sense, as Europeans purchase rail tickets more frequently than airline tickets. Furthermore, the company is seeing rail customers using other Prime products at a high rate, so rail is helping to eDreams widen the moat (1). Lastly, NPS scores for rail customers are especially strong. Given all of this, I imagine that the company will ultimately find that rail customers will have an above average LTVs.

Regarding the new geographies, the company is finding that the new markets have exceptionally high initial household penetration levels, higher net promoter scores, and higher Prime attachment rates compared to their established European markets. This is good news so far, but I look at it a couple of ways. First, we know that we will spend money on these markets next year to get a base level of customers. After the base is built, the Company should enjoy ample free referrals in these markets and the customer acquisition costs will come down. Second, if at any point these markets look like they won’t pan out, the company can just stop the investment in them, which would boost cash flow and earnings in the short term. I don’t think the latter will happen, but if it does, it would not be the end of the world.

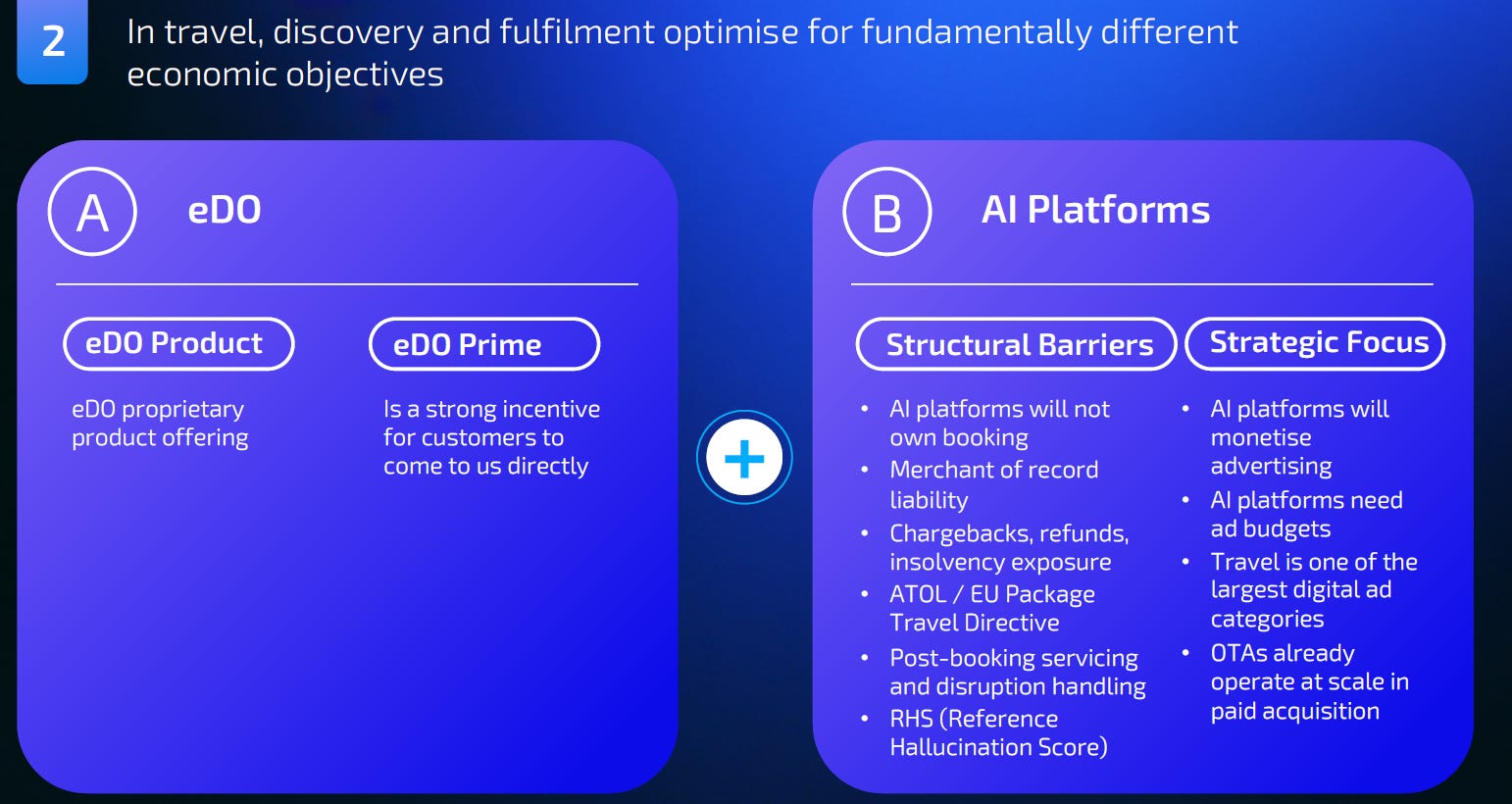

I don’t want to spend too much time discussing the AI threat to eDreams in this article, as the company recently gave a detailed presentation on eDreams long-time use of AI and why the business should not be negatively affected by it (5). I would just leave you with that there are massive structural barriers that prevent AI platforms from disrupting eDreams, furthermore the strategic focus on platforms is closer to the top of the funnel than the plumbing, fulfillment, and customer service component of the travel industry.

The loss of access to the Ryanair content is unfortunate (mostly for consumers, as Ryanair is preventing customers from accessing other travel services and products other than what Ryanair itself offers), but the growth of Prime and the company’s earnings have not been overly impacted by this. The financials will be impacted in the short term by the addition of more frequent payment options for Prime and the new markets and services, but this is setting up long-term growth that probably exceeds that of the plan laid out in the ’25 CMD. Additionally, I do not think that these recent introductions were a direct response to the Ryanair issue. The company had been testing the new services, payment frequency, and geographies for quite some time, so the timing was likely coincidental.

Going Forward

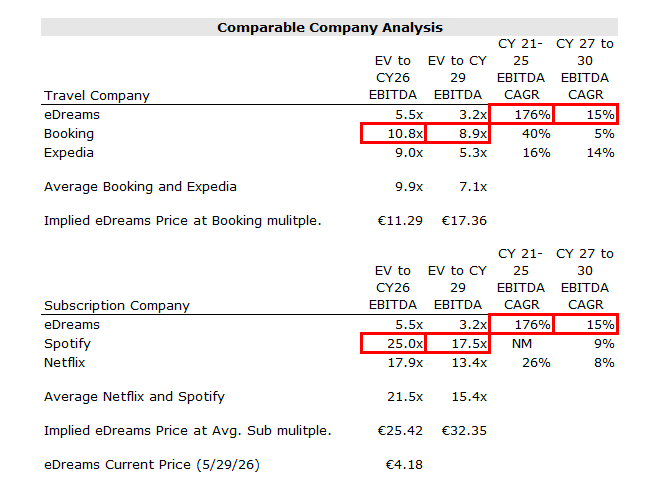

Management rightly makes the point that that at the ’21 CMD, they set out aggressive, long-term plans, which they ultimately achieved despite major and unanticipated headwinds. They are asking investors to believe them again and why shouldn’t they. If they achieve their new plan, they will EBITDA at a 15% CAGR between FY27 and FY30. Their FCF per share will grow even faster as they both de-lever and reduce their share count. Shareholders win just on an earnings growth alone, but shareholders will really win when the earnings growth is combined with a multiple re-rate and share buybacks.

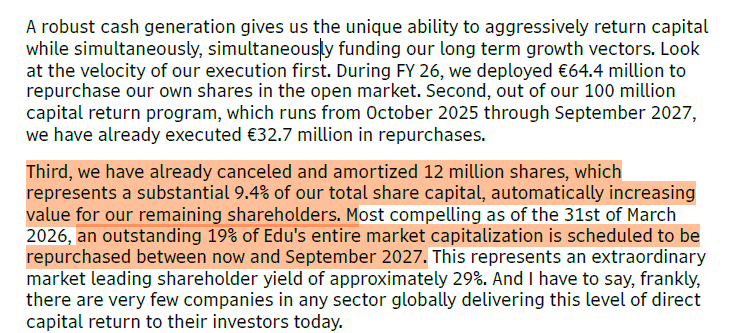

Management is not just asking you to believe them, but they are also putting their money where their mouth is. First, from a capital allocation perspective, they are buying back an ample amount of stock.

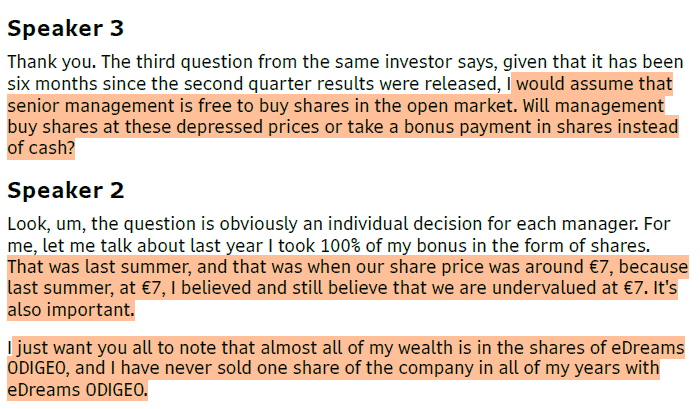

Second, from a share ownership perspective, Dana Dunne, the CEO, was quite forceful when asked about buying additional shares at the current market prices, indicating that he was buying at €7.00, as he thought the price was low and it’s still cheap at €7.00. Also, most of his wealth is in the company and he has never sold one share.

It is disheartening to have a stock price get cut in half in a day. While I understand the concerns the market had in November 2025, clearly the evidence suggests that the concerns were misplaced. The market seems to be agreeing, as the stock is up 22.2% since the Q4 earnings release. Going forward it is exiting to own a cheaply valued stock, that is growing rapidly, buying back ~20% of its market cap in the next 16 months, and is regaining the trust of the market, which should lead to multiple expansion.

Appendix:

(1) https://310value.substack.com/p/applying-nick-sleeps-and-qais-zakarias

(2) https://310value.substack.com/p/unpacking-edreams-capital-markets

(3) https://310value.substack.com/p/ryanairs-256m-fine-may-be-tip-of

(4) Note that the Prime Subscription Plan is still an annual plan, but instead of paying for it up front, you make monthly or quarterly payments.

(5) https://investors.edreamsodigeo.com/English/events-and-presentations/presentations/default.aspx

Disclaimer: Long eDreams, but under no obligation to update position or plans. For entertainment and informational purposes only. Not an recommendation or solicitation to buy or sell any security. Do your own due diligence.

nice post. what do you think of trains as a market? my issue is that unlike flights, trains in europe are controlled quite tightly by national players, this making the need for a marketplace much less.

Airbnb is the leading platform in alternative accommodations, while Booking has a strong position in traditional hotels and travel bundling. eDreams appears to compete primarily with Booking, but what differentiated advantage does it offer that Booking lacks?

The online travel agency business seems to have limited barriers to entry and weak competitive moats, with strong network effects and scale advantages favoring a small number of dominant players. In that context, the market could become increasingly concentrated around leaders such as Airbnb in alternative accommodations and Booking in hotels and broader travel services. eDreams may therefore face challenges in establishing a durable competitive advantage against these larger platforms-> winners takes it all?