Unpacking and Challenging Ammo Inc.’s Separation Plans

Unpacking and Challenging Ammo Inc.’s Separation Plans

Ammo Inc. issued a press release on August 15th (see here: https://feeds.issuerdirect.com/news-release.html?newsid=7446976016611444), in which they announced a plan to separate their e-commerce business from their manufacturing business. This announcement was the beginning of a steep decline in the price of the company’s stock, as it closed near $6.00 per share on August 12th, and it now trades around $3.15 per share. The market seems to think that this is a bad direction for the company, and I agree. Let’s look at management’s rationale for the spin off and my challenges to it.

Strategic Benefits from The Press Release

My Response to Their “Benefits”

Better Positioned to Enhance Shareholder Value: The assertion here is that an e-commerce business and a manufacturing business should be valued differently and implies that having them together causes the company to be valued worse than their sum of the individual parts. It also presupposes that there is no strategic value in having these two businesses together. To these, I submit the following:

Yes, it does make sense that an e-commerce company and a manufacturing company should be valued differently. That said, both these e-commerce and manufacturing businesses are firearms related. Many investors do not want to be invested in such businesses. This cloud over both businesses may overwhelm a benefit that separation would usually provide. I would also point out that having two disparate businesses in a holdco doesn’t always lead a conglomerate discount. Chemed (Ticker: CHE) owns the plumbing services company Roto-Rooter and the hospice provider Vitas. Chemed doesn’t not trade at a conglomerate discount. The likely reason for this is they have adequate disclosures for each business and management is willing to buy large amounts of company stock if the valuation gets too low.

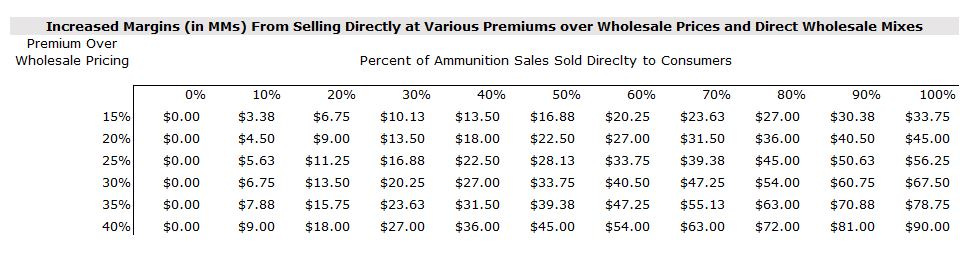

There is an dis-synergy in separating the two businesses as it removes Ammo’s ability to sell ammunition directly to consumers via www.gunbroker.com. Assuming that they sell $225 million in ammunition in a year, and that they could get a 30% premium over wholesale prices by selling direct, if they sold 30% of their ammunition directly to consumers, then the incremental margin to Ammo would be around $20 million. This margin ramps up the more they sell direct. The table below illustratively shows various margin increases at various levels of premium over wholesale pricing and direct/wholesale mixes. With this much margin (profit) to be gained, why separate the businesses?

Enhancement of Brand Strength: This is a bunch of words that looked like they were developed by a public relations firm.

Prioritize Capital Allocation: This makes sense to do if the two businesses have disparate capital goals. I don’t see that here. After years of completing several acquisitions and building a new manufacturing plant, the last thing the manufacturing company needs to do is to do more acquisitions. The capital plans of both businesses should be to support organic growth and return capital to shareholders. Ideally capital should be returned via share repurchases given where the stock is trading; although, a strong argument can be made for instituting a small but growing dividend to increase the size of the prospective shareholder base.

Expand Strategic Opportunities: See above on regarding M&A.

Reinforce and Amplify the Ability to Attract and Retain Top Talent: I agree in the need to do this, but transaction that would destroy shareholder value is not the way to achieve this goal.

Enhanced Strategic Focus with Supporting Resources: Management certainly needs to be enhanced, but it has is hard enough to do this for one company, why try to do it with two?

From a strategic perspective, this does not make sense. To create shareholder value, management needs to spend as much time as possible executing on selling ammunition directly to consumers, as illustrated in the above data table.

Let’s dive into their slides:

Bullet number one, retain ownership in Outdoor Online, and gain ownership of Action Outdoor Sports and at no additional costs.

Well, shareholders already own both, and in a spin scenario, shareholders would be burdened with separate accounting and financing systems, IT systems, public company costs, separate boards of directors, and additional management.

Is the Unanimously Approved by Board bullet true? It could possibly be true that Steve Urvan voted for it and then had a change of heart after seeing the reaction in the stock price. Regarding their capital allocation bulled, I think capital allocation was previously addressed. Regarding the cost control bullet, this can be done without separating the companies, which incurs separate stand-alone company expenses. The companies don’t need to be separate to be nimble.

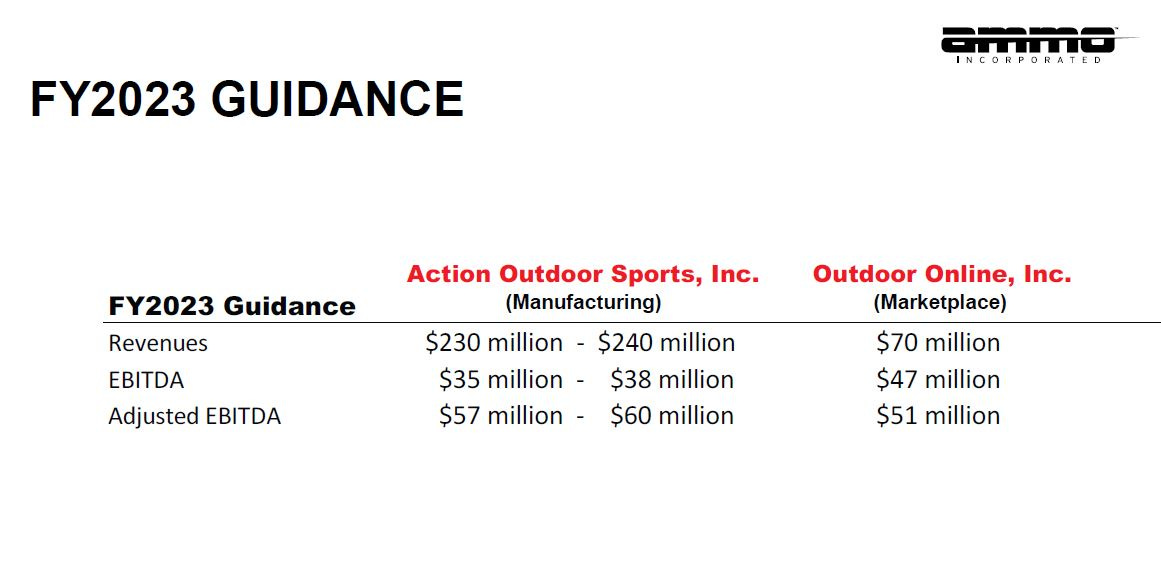

Apparently management has it in their heads that the business is worth $1 billion. They get there by multiplying 15x Gunbroker’s estimated Adjusted EBITDA, and the same with the manufacturing business, then adding the two products. The problem with this is that investors can clearly see the revenue and earnings histories of each of the two businesses and do the math on their own. It is not like having these two businesses together obfuscates the economics and values of each of the businesses. The spin does not solve a problem. What is a problem is what they are using for Adjusted EBITDA. The large spread between EBITDA and Adjusted EBITDA for the manufacturing business tells me that they are likely continuing their practice of adding excise taxes back to get to Adjusted EBITDA. This is ridiculous, as excise taxes is a legitimate expense. Looking at Vista Outdoors, they handle this by excluding excise taxes from their revenue, so it does not even hit their income statement. That seems like an appropriate way to handle it to me. Using add-backs such as this hurts management’s credibility and that may be weighing more on the stock than any holdco discount.

Conclusion:

The case for separating the two businesses is weak in my mind. First, it will mean that each business will have to bear redundant stand-alone costs as separate public companies. Second, I don’t think the business suffers from a conglomerate discount, and if it did, the first step to deal with this is by repurchasing stock. Third, I think management has a credibility issue, and the separation will not solve that. Finally, immense shareholder value can be created by selling Ammo’s products directly to consumers, and the separation would make that less compelling.