Two Companies Marked Safe from the SaaS Apocalypse

LandBridge and Texas Pacific are not only safe, but are likely AI beneficiaries.

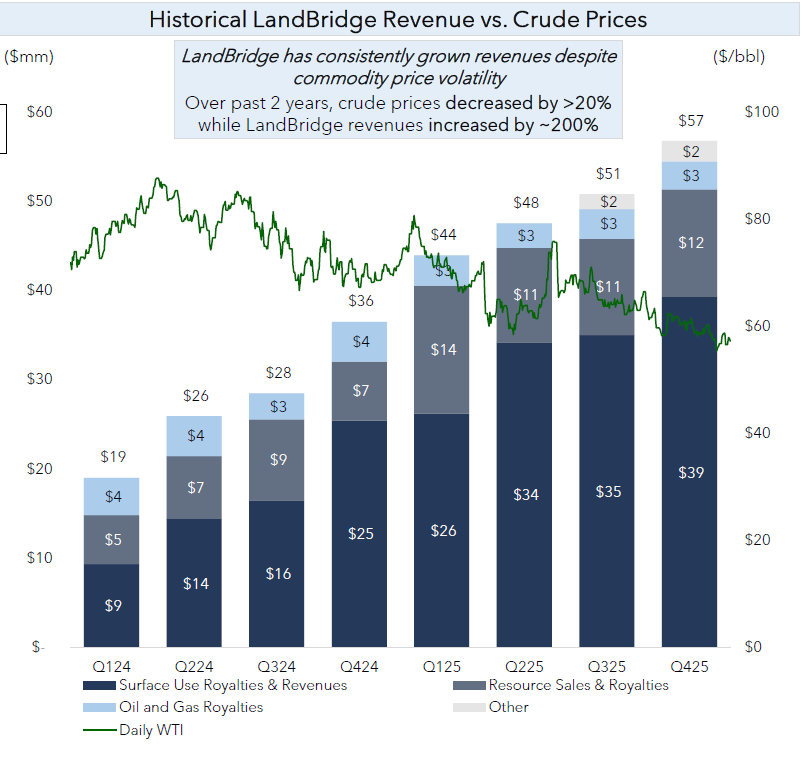

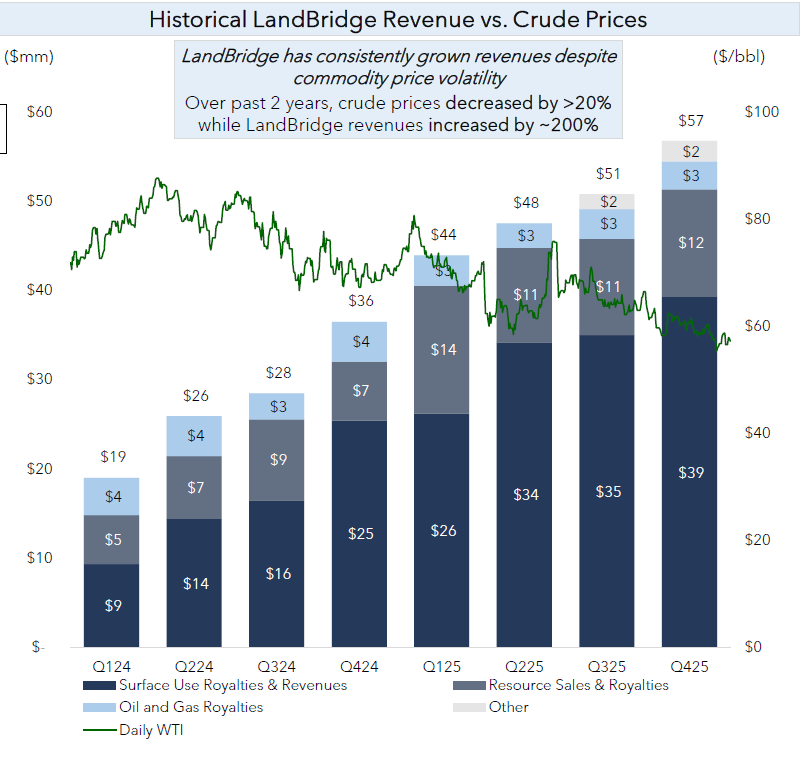

Given LandBridge’s earnings release this week and Texas Pacific Land Corporation’s (“TPL”) last week I thought it was a good time for another article on them. Not only did both companies report strong fourth quarter earnings, but also both had strong stock price appreciations during a week when many companies sold off following the Citrini AI article (1). Additionally, I received several calls from fellow investors who are doing work on one or both companies; I heard the thesis of some shorts; and I heard some comments on these companies that are a bit off, to be kind. While many companies and industries have an uncertain future considering AI, LandBridge and TPL likely have bright futures and could possibly be AI beneficiaries. So, let’s dive into what they are, how they make money, how they differ from mineral royalty companies, some common misconceptions, and how they differ from each other.

Texas Pacific Land Corporation

TPL went public in 1888 as a trust. It was formed out of the bankruptcy of the Texas and Pacific Railroad. At the time, it was left with 3.5 million acres land and mineral interests in Texas. The job of its trustees was to oversee the trust in selling the land and returning money to unit holders (shareholders) via unit repurchases and dividends. For most of its life it made money by providing easements to conventional oil and gas operators operating on TPL’s surface acreage, collecting royalties from its mineral interests, leasing land to cattle ranchers, and selling off land. The cash it generated was returned to unit holders. Then came fracking, which made TPL’s unit holders some of the luckiest shareholders on the face of the Earth. The last decade for TPL has been interesting and brought substantial changes, such as converting the trust to a c-corp., a massive expansion of headcount, and a move from being a collector of checks into an operator of businesses. Let’s move directly to what TPL does now, but if you are interested in its history, I wrote an article (2) on TPL’s capital allocation practices which covers some history and there is a podcast that goes into it (3). If you really have some time, the TPL Blog is worth reading (4). At present TPL has ~888,200 acres of land. A map of their acreage is below (5). Notice that most of the land is in a checkerboard fashion, which was how it was given to it by the government when the railroad was trying to be built. They have sold, swapped, and acquired land, which is likely why you see some land that is contiguous and not in the checkerboard fashion.

How TPL Makes Money

Mineral Royalties: TPL has 224,000 royalty acres primarily in the Permian Basin. These royalty interests are non-participating, meaning they do not need to write checks to help fund the oil and gas development, they just cash the checks that are sent to them. Mineral royalties represent 46% of TPL’s revenue. This revenue stream is arguably lower quality than other streams and is volatile, as it is directly tied to the price of oil. Additionally, once the minerals are extracted and the royalty on them is paid, they are gone forever. So, to have an ongoing mineral royalty business, the depleted minerals will at some point need to be replaced.

Source Water Sales: TPL invested and built out a massive source (brackish) water business in the last decade. This business is currently 29% of TPL’s revenue (17% a year ago). This business is tied to new drilling activities, so it is more volatile than TPL’s next business, produced water.

Produced Water Royalties: Given TPL’s extensive surface land ownership, it has land that is suitable for some salt-water disposal wells (“SWD”). TPL allows produced water disposal companies to deposit produced water into wells on its property. TPL gets paid per barrel royalties. Produced water royalties are 16% of revenue. Produced water royalties are less exposed to new drilling activities (6, 7, 8) and are therefore a higher-quality revenue stream.

Surface Easements: TPL gets paid easements for access to its properties by e&p companies, which would include easements for drill pads; roads; power lines; oil, gas, and produced water pipelines. Additionally, it gets paid for materials extracted from its surface such as frac sand and caliche. Surface easements are, for the most part, higher quality. Surface use easements represent 10% of revenue.

Land Sales: Occasionally, TPL will sell some of its surface acreage, but this activity is sporadic. In Q4 2025, there were no sales.

LandBridge

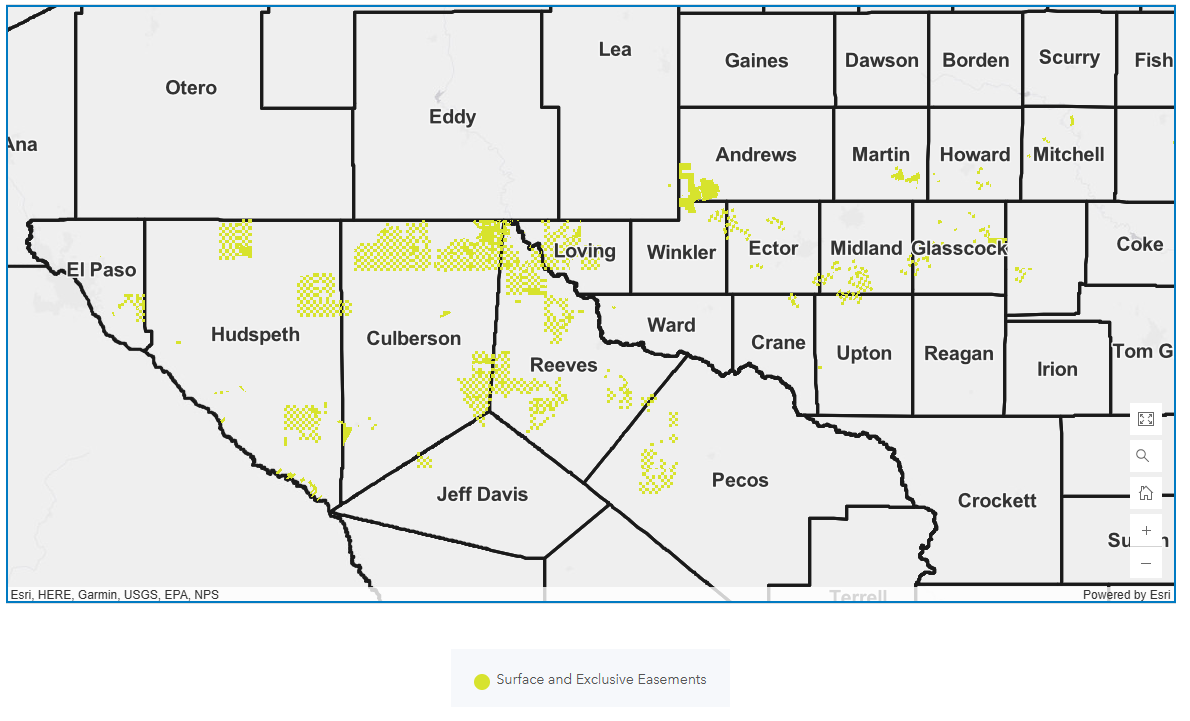

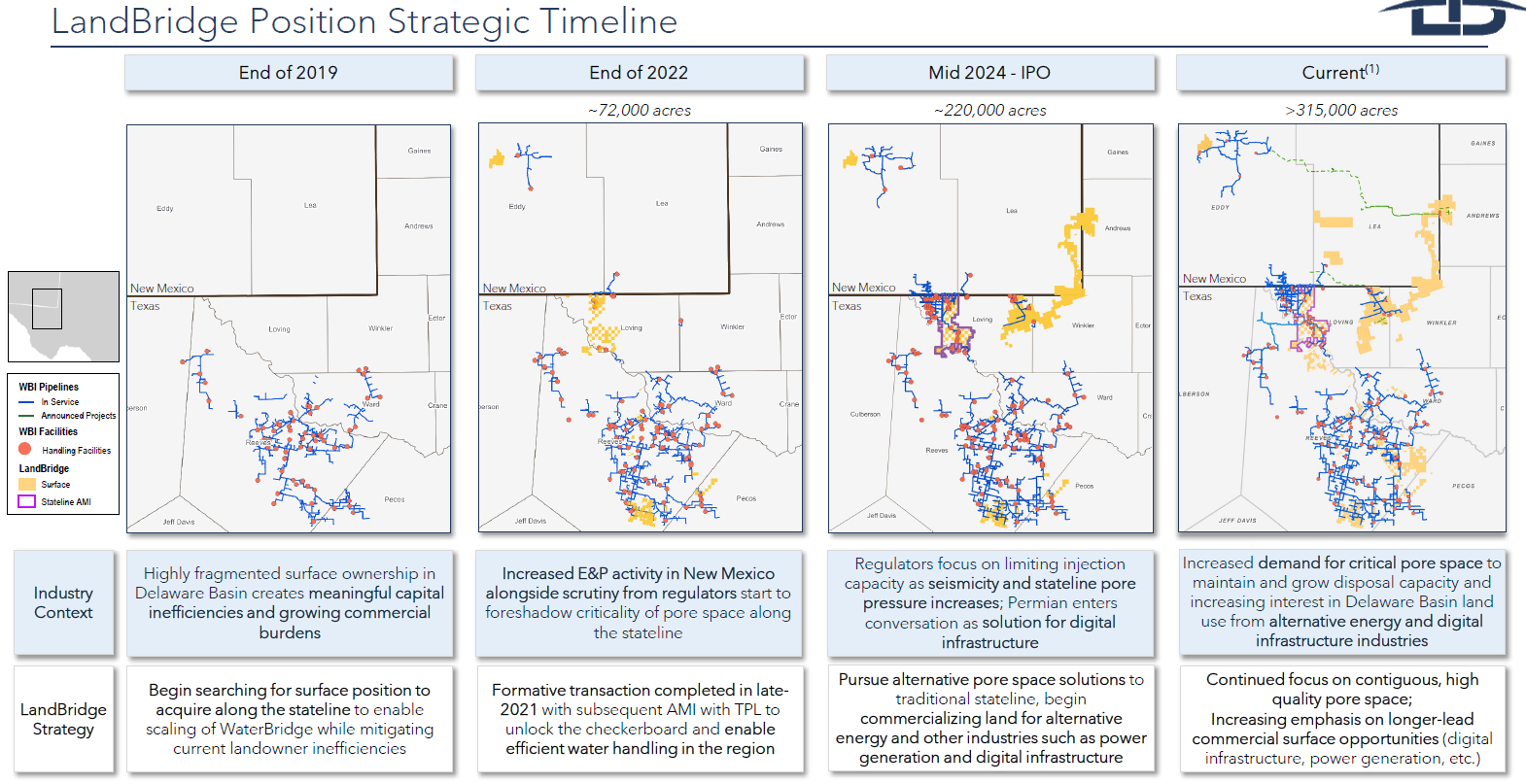

LandBridge was formed, initially, to help scale its sister company, WaterBridge. By 2022, it acquired its first acreage ending the year with 72,000 acres and an Area of Mutual Interest (“AMI”) with TPL. The initial transaction enabled efficient water handling for WaterBridge. By 2024, regulators became concerned with seismicity and issues with pore space pressurization. Pore space is subsurface space suitable for SWD wells. LandBridge expanded their land holdings to increase the amount of incremental pore space and to acquire critical locations along the New Mexico state line. New Mexico’s produced water often flows into Texas for disposal, so ownership of land along the border results in a low-cost moat for LandBridge / WaterBridge, as each new property produced water must cross is an opportunity for a property owner to extract a toll. Lastly, the opportunity to put digital infrastructure assets in the Permian Basin became a possibility and LandBridge acquired land in anticipation of this thesis playing out. Such land needs to be close to a natural gas hub and be of sufficient size to house and LLM data center campus, around 2,000 acres. LandBridge now manages 315,000 surface acres.

When LandBridge went public in June of 2024, many investors thought that LandBridge was a mini TPL. That was an attractive notion. TPL has been a stellar performer, why not invest in another TPL, especially at a lower multiple? However, that notion is not entirely accurate. First, while LandBridge has some mineral interests, these interests are not a focus and are incidental. LandBridge is not actively acquiring mineral interests, they buy it only if it comes with surface land they are buying, with the surface land being the primary driver of transaction. The land they purchase is purposely driven to support WaterBridge’s / LandBridge’s produced water business, as well as LandBridge’s digital infrastructure initiative. The below shows the progress of their landownership over time. It is shocking that other players, perhaps better capitalized players, were asleep at the wheel and allowed LandBridge to acquire miles and miles of Texas Stateline land.

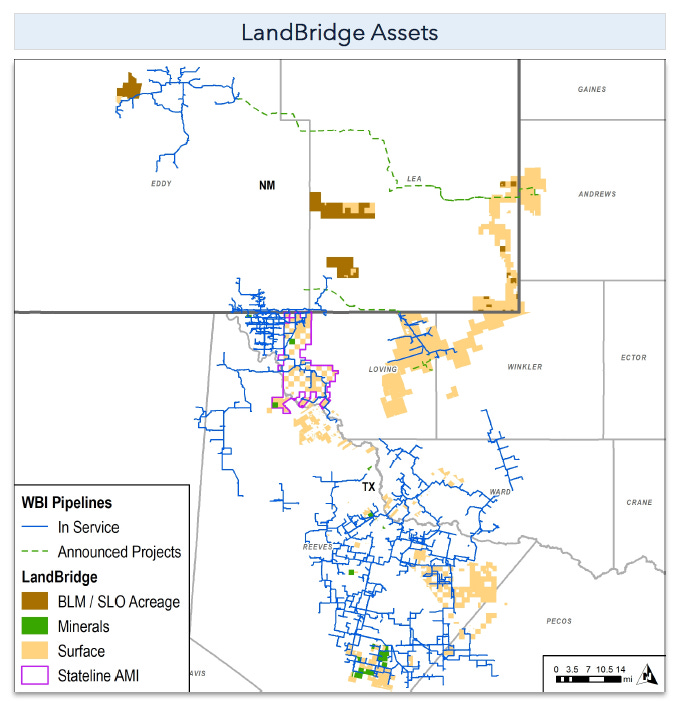

The map below shows LandBridge’s assets up close and WaterBridge’s Permian network. Recall, that water from New Mexico flows south and east into Texas and that each new property it crosses is an opportunity to be charged a toll. LandBridge’s AMI and Stateline landownership is a figurative moat around its business. For more on this see this article (9).

How LandBridge Makes Money

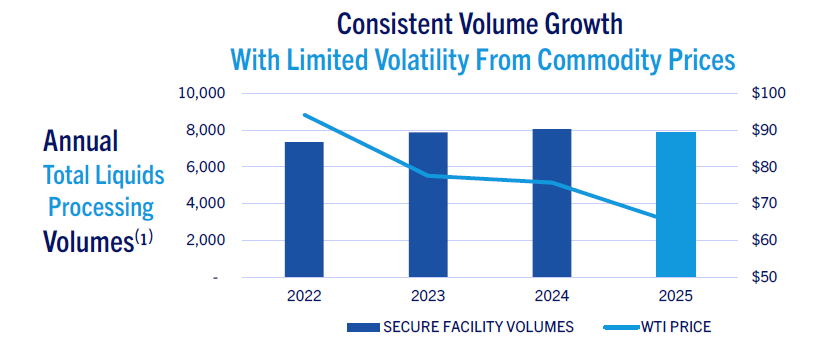

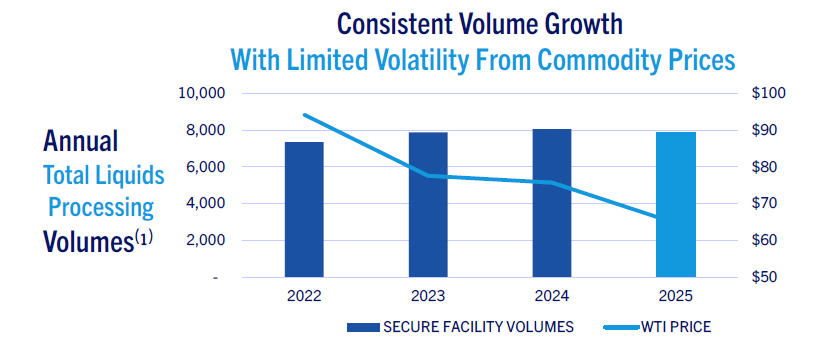

Surface Use Royalties: This is a combination of surface easements and produced water royalties (although mostly produced water royalties). It represents 69% of LandBridge’s revenue – 73% if you include deficiencies recognized under minimum revenue contracts. As previously mentioned, surface use and produced water easements are resilient and therefore, high-quality revenue streams (10, 11)

Resource Sales: Resource are sales of source water, caliche, frac sand, etc. These sales represent 21% of total revenue.

Mineral Royalties: As mentioned, LandBridge acquires mineral interests incidentally and is not focused on it. Minerals represent 6% of total revenue.

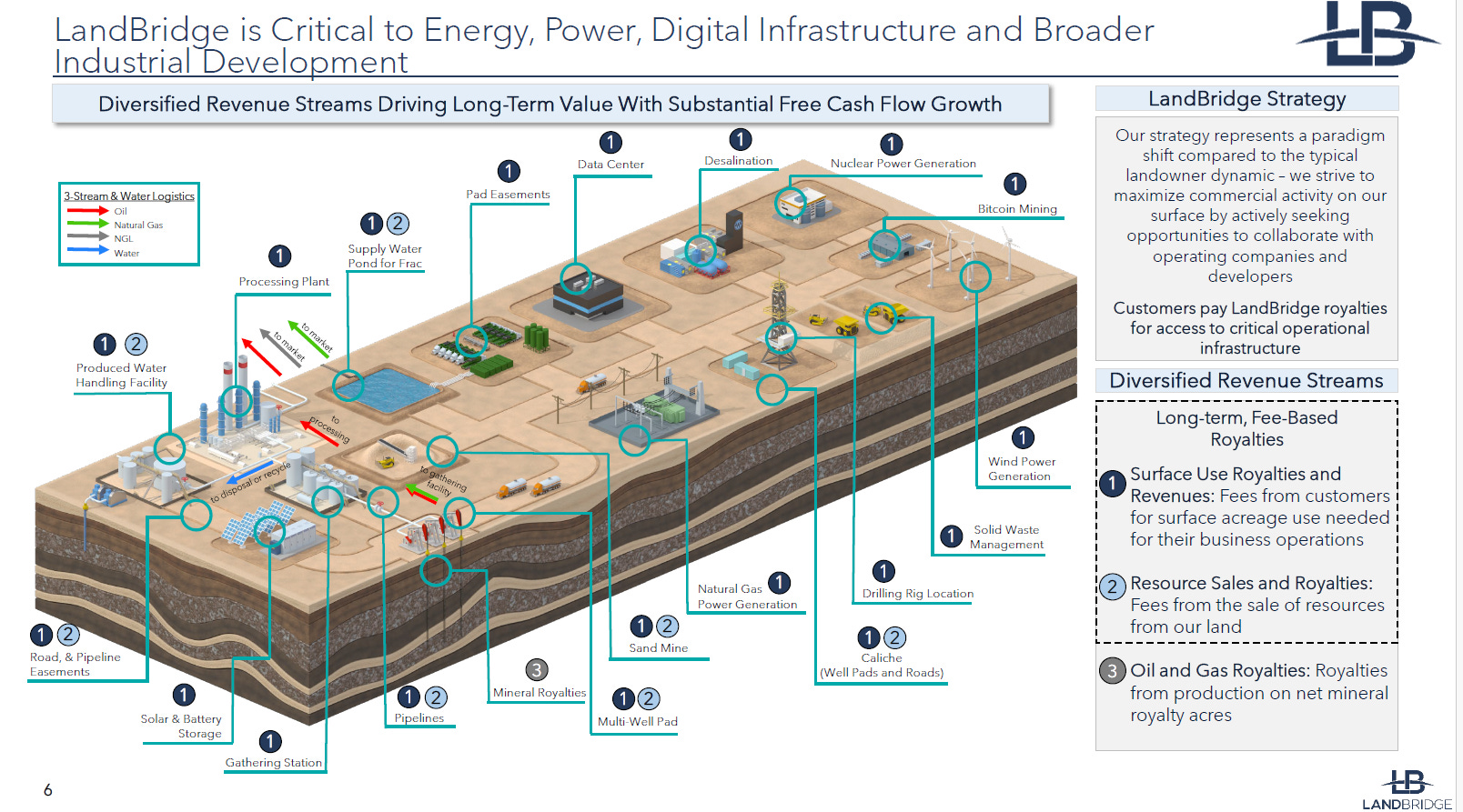

LandBridge is focused on maximizing the value of its surface acreage through ownership of pore space, produced water pipeline easements, and next generation uses such as data centers, solar fields, batter farms, and power generation facilities. The below picture shows various ways management plans to maximize the value of LandBridge’s acreage.

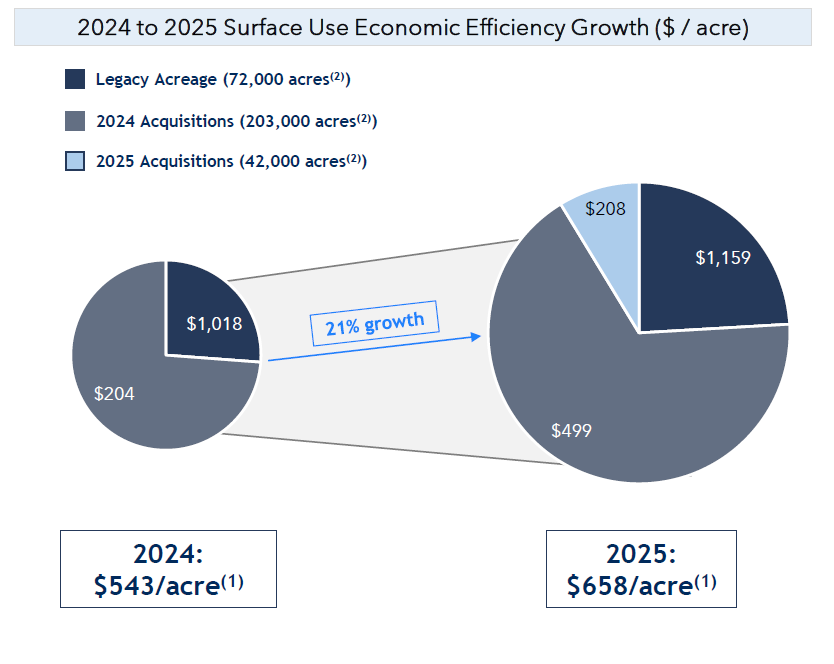

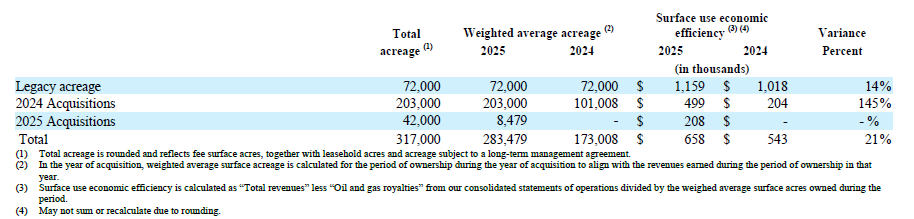

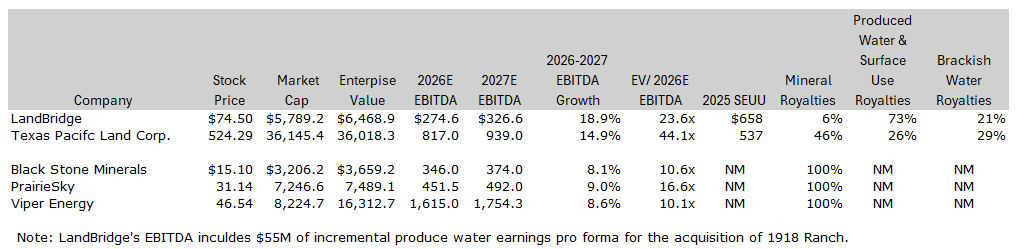

Surface Use Economic Efficiency (“SUEE”) is how management rates their maximization of surface acres value. It is done on an overall basis, as in the picture below. It is also done by vintage of property purchased, as shown in the chart. The concept of measuring SUEE is not perfect, but it is interesting, and directionally good. It also shows that management is willing to show in black and white the results of both their capital allocation decisions and their operational acumen. The caveat is that not all land in the Permian Basin is the same. Not all land would be good for data center use. Not all land has valuable pore space. Therefore, this metric does paint a picture with a broad brush, but no metric is perfect. In addition to this, management can rate their business by revenue source. For example, we have x mbpd of pore space in use and we are getting paid y; we have z amount of incremental pore space which we expect to use over the next several years. The same can be done with data centers. Setting the caveat aside, increasing the SUEE of the 2024 acquisitions by 145% in one year and the overall property portfolio by 21% is objectively good. By comparison, LandBridge’s SUEE per acre is $658, while TPL’s is $437. So, LandBridge is SUEE is 50% higher than TPL’s.

The Data Center Thesis

I don’t want to get too in depth on the data center thesis in this article. I have covered it in the past in my article on LandBridge’s pore space (13) and three specific articles covering data centers in the Permian Basin. The latest goes in depth on Chevron’s plans to build a 2.5GW power plant in Reeves County (14). A quick update on that article. Chevron has received the requisite tax abatement from Reeves County. All that Chevron needs to move forward is an off-take agreement. It would not surprise me if the TPL affiliated Bolt Data and Energy were working hard to be the off-take provider to Chevron, as the power plant is planning to be located on 7,000 acres of land in Reeves County. A good chunk of that land is TPL’s. Lastly, LandBridge also has a power plant project in the works as well.

There will be several ways for LandBridge and TPL to monetize the data center opportunity. One way that was highlighted on TPL’s Q4 25 earnings call is selling water for use in cooling the data center and the production of power. James Davolos from Horizon Kinetics did some good work on putting numbers to how much water a data center will consume in both its cooling and power generation needs (12). Investors can put a per barrel revenue assumption for that water that TPL and / or LandBridge can make, but to save you the reading of Horizon Kinetics Commentary, the numbers can get big quick for both companies. I would note that there are only two places for the water to come from. It can come from an aquifer, or it can from recycled produced water. Maybe some of the early projects will use water from an aquifer, but the political blow back will probably drive the use of cleaned produced water. While there are a handful of produced water pipelines in Reeves County near the proposed Chevron power plant site, WaterBridge likely has the densest water network in the county. Given TPL’s valuation (recent Iran events excluded) upside for data centers is likely somewhat factored into the price of the stock. Although, LandBridge’s stock price likely hasn’t factored in much upside from data centers, given the value of LandBridge’s pore space (13).

Valuation

One common misconception that investors have is that TPL and LandBridge are “royalty business”. Yes, they get paid royalties, but it is not all mineral royalties. As mentioned, mineral royalties need to be replaced, which is why you see mineral companies trading around 10x EBITDA. Now PrairieSky trades at a higher multiple, but perhaps that is given the size of its mineral portfolio. Maybe the same argument can be made for TPL, that its royalties are worth mid-teens EBITDA. However, LandBridge and TPL own higher-quality revenue streams than mineral royalties, with LandBridge having the better mix of the two. Hence, that is why LandBridge and TPL trade higher than mineral royalty companies. Relatedly, I often hear that the short thesis on these companies is that the shorts do not believe the data center thesis and if you remove that, these companies should trade inline with royalty companies, so 10x. But these businesses are not mineral royalty companies, and that is the flaw in this short narrative.

Conclusion

Overall, LandBridge and Texas Pacific are unique and excellent businesses. They should be immune from AI headwinds. They may in fact be beneficiaries if AI data centers go to the Permian Basin, and it seems increasingly likely that this will occur. Even if data centers are not going to the Permian Basin, AI data centers will increase the demand for natural gas, which benefits both companies. While these companies are similar, they also have their differences. TPL’s management is spending massive amounts of shareholder capital to increase their royalty portfolio. This decision baffles me given that TPL has a limited edge in making these acquisitions and that mineral royalties are their lowest quality revenue stream. LandBridge’s management, on the other hand, is strategically purchasing surface acreage and maximizing the value of those acres. While both companies deserve to trade a premium to mineral royalty companies, given LandBridge’s higher growth rate and higher-quality revenue streams, it should trade at premium to TPL.

Appendix

3:10 Value: Drilling Down on Disposal - Produced Water's Parallels with Municipal Waste

LandBridge’s Chart on Revenue at Various Oil Prices

11. Secure Waste Infrastructure Corp.’s Chart on Liquid Volumes at Various Oil Prices

12. Horizon Kinetic's Q4 '25 Commentary

Disclaimer: Not financial advice. Not a solicitation to buy or sell any security. For informational and entertainment purposes only. Do your own due diligence. Long both companies as of date of publishing, but under no obligation to update positions.

Great post!

Don't forget WaterBridge