Digital Bridge: Secular Growth Tailwinds Squared

$DBRG has multiple secular growth tailwinds that provide resistance to recessionary forces.

Digital Bridge Overview:

Digital Bridge is the former Colony Capital, which shifted from being a REIT that tried to be everything to everyone by owning hospitality, industrial, healthcare assets, etc., to a REIT and investment management business focused on investing in digital infrastructure assets (data centers, small cells, fiber, cell towers, edge installations, etc.). Recently, the company announced that it would convert from a REIT to a c-corp.

Digital Bridge is comprised of 3 businesses:

Digital Operating (DO): DO invests DBRG’s balance sheet capital in stable, lower-risk digital real estate (currently data centers, but likely towers in the future, and primarily domestic) producing consistent free cash flows. Note that the conversion to a c-corp. shows the direction DBRG is probably going. They will likely seed new strategies on balance sheet and move them to Digital Investment Management once they are established.

Digital Investment Management (DI): DI invests third-party capital in a broader pool of higher-growing digital assets (fiber, small cells, data centers, towers, with significant international exposure). DI has $45B in digital asset AUM - excluding the recently announced AMP transaction.

Other Investments: Other includes DBRG’s equity investments in its Digital IM vehicles, Digital Liquid Strategies, and seed investments for future DI vehicles. Additionally, Other contains stakes in legacy assets such as their ~25% stake in BrightSpire Capital (BRSP), formerly Colony Credit.

Management believes that the services of DBRG’s portfolio companies can be offered to a customer together and there is value in being part of DBRG’s ecosystem. This point may confuse investors, as it is hard to underwrite. I think that one can look at their portfolio company offerings/investments individually and value DBRG accordingly. Although, if management is correct, then that is an additional benefit to DBRG and ultimately its shareholders.

Management, both internal at DBRG and external at DI’s and DO’s portfolio companies, is an impressive group of executives with deep domain expertise.

Digital Bridge Investment Thesis

Looks to be the best investment and operating teams in the digital industry.

KKR, Brookfield, Blackstone, etc. may have a handful of professional working on digital infrastructure investments. Pre the AMP transaction, DBRG had 197 employees working on digital infrastructure investments globally. They are picking up a mid-market infrastructure team with AMP.

CEO and CIO both have long histories of creating value in the space for investors.

Digital IM should benefit from LPs movement towards increased exposure to alternatives, as well as exposure to secular-growth industries.

While there are many publicly traded private equity firms, DBRG is the only firm focused on data demand driven industries such as: 5G, accelerated digitization, development of data-driven technologies, etc.

Substantial capital deployment opportunities at DO and DI should drive growth.

The company has a substantial amount of liquidity on balance sheet to deploy from the sale of the legacy Colony assets.

Recurring, Long-Term Cash Flow in DO and DI

Secular growing business should provide a stable and long-term cash flow growth regardless of macro headwinds.

DBRG gets 100% (less employees’ salaries and expenses) on base asset management fees.

Diversified exposure across the entire digital infrastructure landscape with possible synergies from such exposure.

Additionally, the diversified footprint allows DBRG to deploy capital to areas (geographic, industry sector) of the highest return and gives them the option of buying or building.

Management team with substantial incentives to create shareholder value.

Valuation looks attractive using conservative assumptions.

DBRG seems to recently be suffering from forced selling as REIT only investors are being forced to exit it.

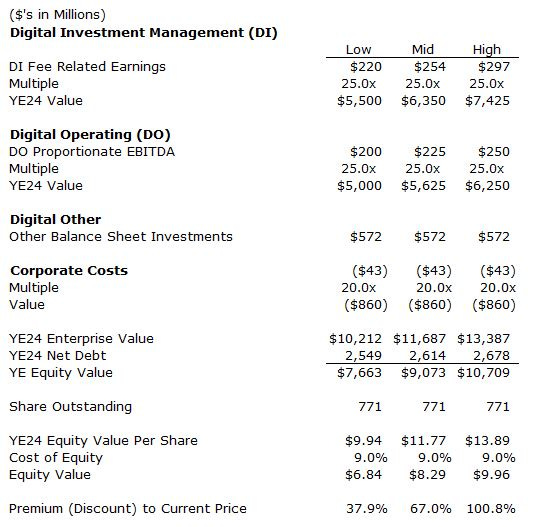

Sum-of-the-Parts Valuation

Assumptions:

The valuation excludes value from carried interest, of which DBRG gets 35% of the carry for large funds and 40% for smaller products.

DI fee estimates are management’s estimates for FRE plus

Low: No additional fund raised for AMP Platform.

Mid: $3.0B in AUM raised for AMP Platform.

High: $5.25B in AUM raised for AMP Platform.

Note: FEEUM growth at Low scenario over the next four years comes to a 16.1% CAGR.

Investment Philosophy:

Digital Bridge’s investment philosophy comes from the investment principals the CEO, and some of the other team members, used while building Global Tower Partners (“GTP”). At GTP their beliefs were: 1) People create alpha; 2) build an M&A engine; 3) organic growth comes from listening to customers; 4) capture information and use it; and 5) finance the asset class.

Digital Bridge wants to invest in areas where they have an edge. They want durable cash flows with secular growth driven by digital themes such as 5G, AI, and cloud-based apps.

Digital Bridge focuses on:

People: established operators, investors, and thought leaders.

Best-in-class assets: mission critical and hard-to-replicate infrastructure.

Disciplined framework:

Four Corners of Asset Selection:

Market dynamics: stable markets with a catalyst for near-term digital infrastructure investments with downside protections for owners.

Asset quality: focus on hard to replicate and high switching costs.

Contract quality.

Alpha creation: drive outperformance with human capital decisions, direct operating experience, back-office systems, differentiated M&A program, and dynamic balance sheet management.

Operational excellence: emphasis on strong organic growth, extensive greenfield expertise, and high ESG standards

Proprietary deal flow: focus on brownfield, greenfield, and new white sheet business plans and carveouts that avoid auctions. Note that every private equity firm talks about proprietary deal flow. In this case, I believe them. See the AMP Case Study below.

Products: flexible and creative solutions across the capital structure (part of how they get proprietary deals).

Prudent leverage: appropriate amounts of leverage used for various transactions.

Digital IM’s Fee Equity Under Management (FEEUM)

FEEUM comes from their flagship funds, liquid funds, and co-investments. In addition, credit (second-lien or skill capital), ventures, and a core fund were added in 2022. Note, core targets 10- to 12-year investments yielding 10% to 12% returns. Core is different than credit and was established to respond to requests from institutional investors.

Management’s goal (pre-AMP announcement) for AUM is to hit $100B in the next 5 years and their goal for FEEUM is to be $40B to $50B inside of 4 to 5 years.

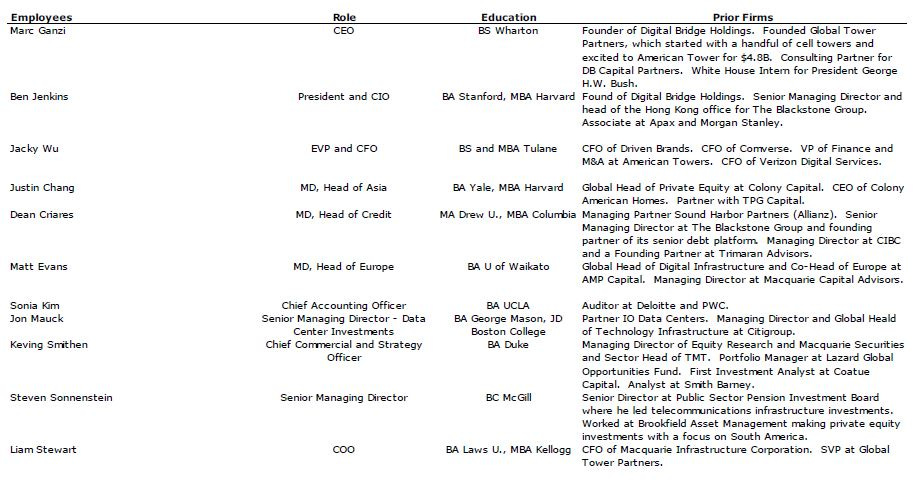

Management

Digital Bridge’s management and investment team have impressive backgrounds at such organizations as: GTP, The White House, Blackstone Group, Apax, TPG Capital, Brookfield Asset Management, Macquarie, Lazard, and Coatue.

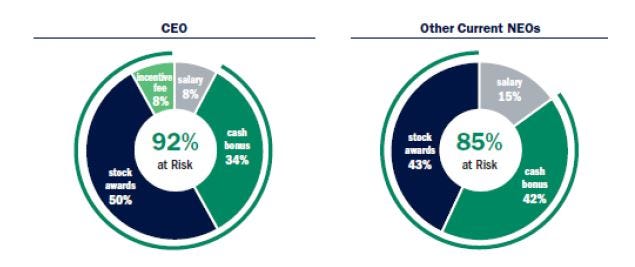

Management has ample at-risk compensation. Below is the various corporate compensation for the CEO and other officers. Furthermore, the investment team receives 60% to 65% of the carried interest of DBRG’s funds. Lastly, as part of his compensation, the CEO will receive $100MM bonus payment should the stock trade above $10.00 per share for 90 consecutive days from now through 2024.

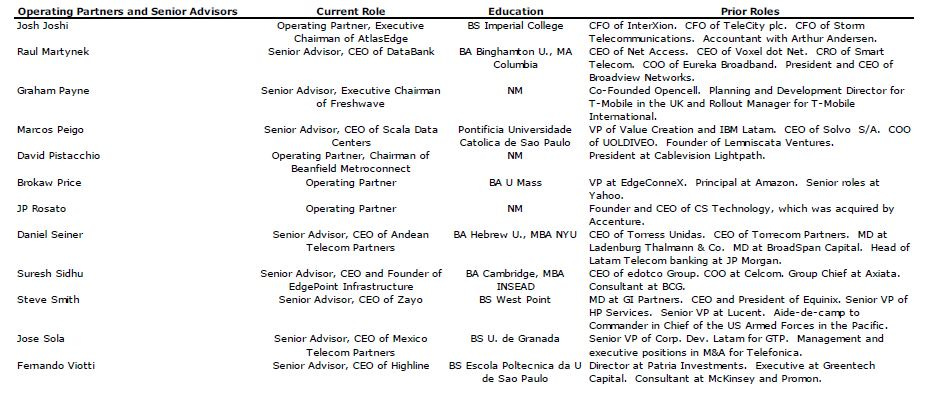

Operating Partners and Portfolio Company CEOs

Not only is Digital Bridge’s management and investment team impressive, but also the leaders of their portfolio companies are equally impressive. Their portfolio company leaders come from organizations such as: Equinix (former CEO), TeleCity (former CFO), InterXion (former CFO), Digital Realty (former CEO), GI Partners (Founder), Verizon, HPE, IBM, Silver Lake, Level 3, GTP (former President and COO), Zayo, Sprint, EdgeConnex, Amazon, McKinsey, BCG, JP Morgan (Head of Latam Telecom), and Salomon Brothers.

AMP Case Study

Overview:

DBRG announced the acquisition AMP International Equity business. AMP has $5.5B in fee-earnings assets in two funds. The strategy employs 25 professionals. It is additive to DBRG as DBRG did not have a mid-market solution.

Opportunity: AMP’s business was reportedly in disarray, and they have been selling off business lines. Rumors are that LPs were discontented. AMP decided to sell the business. DBRG competed with a large, blue-chip private equity fund.

Impressive Purchase Price through Problem Solving: DBRG paid $192MM or 8.4x FRE, which is essentially runoff value. The PE competition tried to buy only the assets from AMP, leaving AMP with an investment team that it would no longer need and would have to be terminated - probably paid to leave. DBRG offered to take the whole business, thus providing a solution to the seller.

Value Creation: FRE margin at AMP is 36%. DBRG should be able to get margins to 50%, which is closer to industry standards. Additionally, DBRG can raise additional funds for the AMP platform (if they do, it will generate an earnout for AMP). DBRG should be able to generate revenue synergies by offering legacy AMP LPs access to DBRG’s other funds, while it offers its current LPs access to future AMP (DBRG middle-market infrastructure) funds.

Risks and Mitigants:

Overall, DBRG’s specialization on digital assets should mitigate risks as domain expertise will likely increase the chances of investment success.

Rotation into digital assets must continue.

Created data grew at a 39.7% CAGR from 2010-2021 and is expected to grow at a 23.0% CAGR through 2025.

DBRG’s investment team must be able to find attractive assets at reasonable prices.

DBRG has a deep team with a long history of investing in the space.

Furthermore, their geographic and sector diversity gives them the best options for allocating capital to the areas most starved of it. Additionally, they have the ability to buy or build, which provides a pressure valve on an overheated market for assets.

DBRG’s operations team needs to successfully oversee the growth of investments.

DBRG team members have successfully grown businesses.

Inflation could increase construction costs.

Development yields are protected with contract pricing flow throughs; asset values rise with inflation; digital infrastructure has a low labor intensity.

Supply chain issues could cause construction delays.

Mission-critical nature of digital infrastructure keeps disruptions to a minimum. Long-standing supplier relationships and scale of DBRG also reduce supply chain disruptions.

Geopolitics elevate Europe’s risks and energy prices.

Power costs are a pass through to customers. No Ukraine nor Russian exposure.

Interest rates impact portfolio company and corporate borrowing costs.

100% of corporate and 83% of portfolio company debt is fixed rate. Portfolio is diversified and prudently financed. DBRG’s team is cutting edge when it comes to innovative financial solutions. They were the first to securitize cell tower cash flows, and recently did the same with investment management fees.

Reliance on third-party capital.

There is a migration towards alternative assets and to digital assets.

Potential departures of investment managers.

Managers are appropriately compensated and likely at the best platform to execute digital infrastructure investments.

The GAAP accounting is complex, which renders the 3 main financial statements useless.

Institutional investors that invest in alternative investment managers are used to similar complexities and using supplemental reporting of these types of businesses.

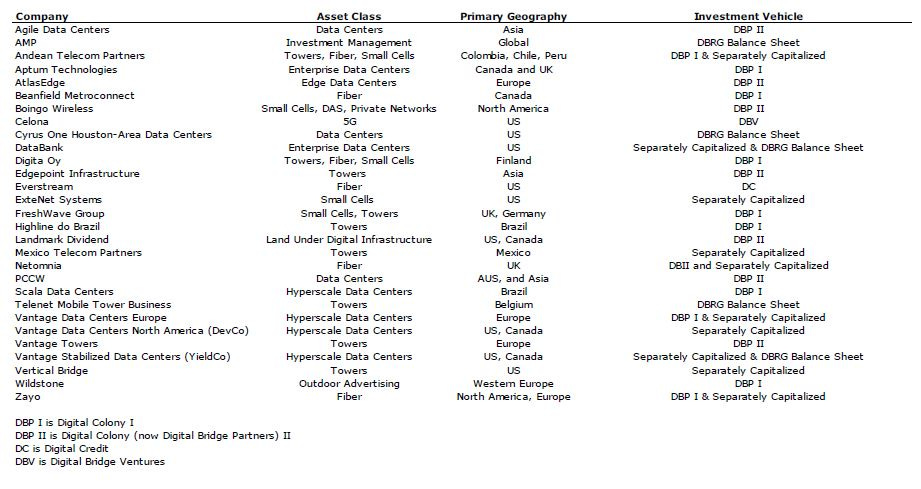

Portfolio Companies

Note: this excludes the recently announced Switch transaction.

Disclaimer: for entertainment purposes only. This is not investment advice nor is this a solicitation to invest in any security. Do your own due diligence.